For anyone who cares about beneficial ownership transparency, the spotlight should be on the EU—where public beneficial ownership registers became mandatory in 2020—and Germany, that is struggling with the issue of anonymous real estate ownership in the face of a looming FATF review and a public alarmed by exploding prices partly due to an influx of anonymous international investment. Later than the UK, Denmark, or Luxembourg but just on time for the EU directive, Germany made its beneficial ownership register public early 2020 and has become one of the first countries worldwide to mandate foreign real estate buyers to register in the local beneficial ownership register.

A new study from the Rosa-Luxemburg-Stiftung tracing the ownership of more than 400 companies owning real estate in Berlin through public and commercial registers worldwide—including the German and other European beneficial ownership registers—concludes that nearly one third are still anonymous, and transparency remains an illusion. With 15 illustrative examples, it shows how implementation and enforcement of beneficial ownership transparency failed in Germany (and other European registers) and why the EU definition of beneficial ownership remains fundamentally flawed in practice.

When the German parliament discussed the implementation of the EU’s fifth anti money-laundering directive, most politicians, experts, and the public agreed. The national risk analysis and the financial intelligence unit had identified real estate as a major risk area for money laundering, and the State Secretary from the Finance Ministry asked parliamentarians for additional ideas particularly in the area of real estate. A prosecutor from Berlin pointedly reminded the parliamentarians that anyone who buys a house in Berlin using a company from any of the secrecy jurisdictions stays out of the law’s reach, because prosecutors have no way of determining the real owners. And last but not least, alarmed by exploding purchase prices and rents, many tenants are no longer willing to accept anonymous investors and dirty money. Soon, the press began to take notice. These days, everyone wants to know: who owns our cities?

Besides opening the beneficial ownership register to the public (as foreseen in the EU directive), parliament passed an amendment that obliges any company from outside the EU wanting to buy real estate in Germany to register in the beneficial ownership register and another one allowing—or forcing—notaries and real estate agents to face increased scrutiny in real estate transactions.

Yet despite these efforts, the Rosa-Luxemburg-Stiftung’s study shows that answering the question of “who owns Berlin?” remains impossible for two reasons[1]:

- The German beneficial ownership register was badly done and is not enforced successfully.

- The idea and definition of beneficial ownership in the EU and FATF guidelines is deeply flawed.

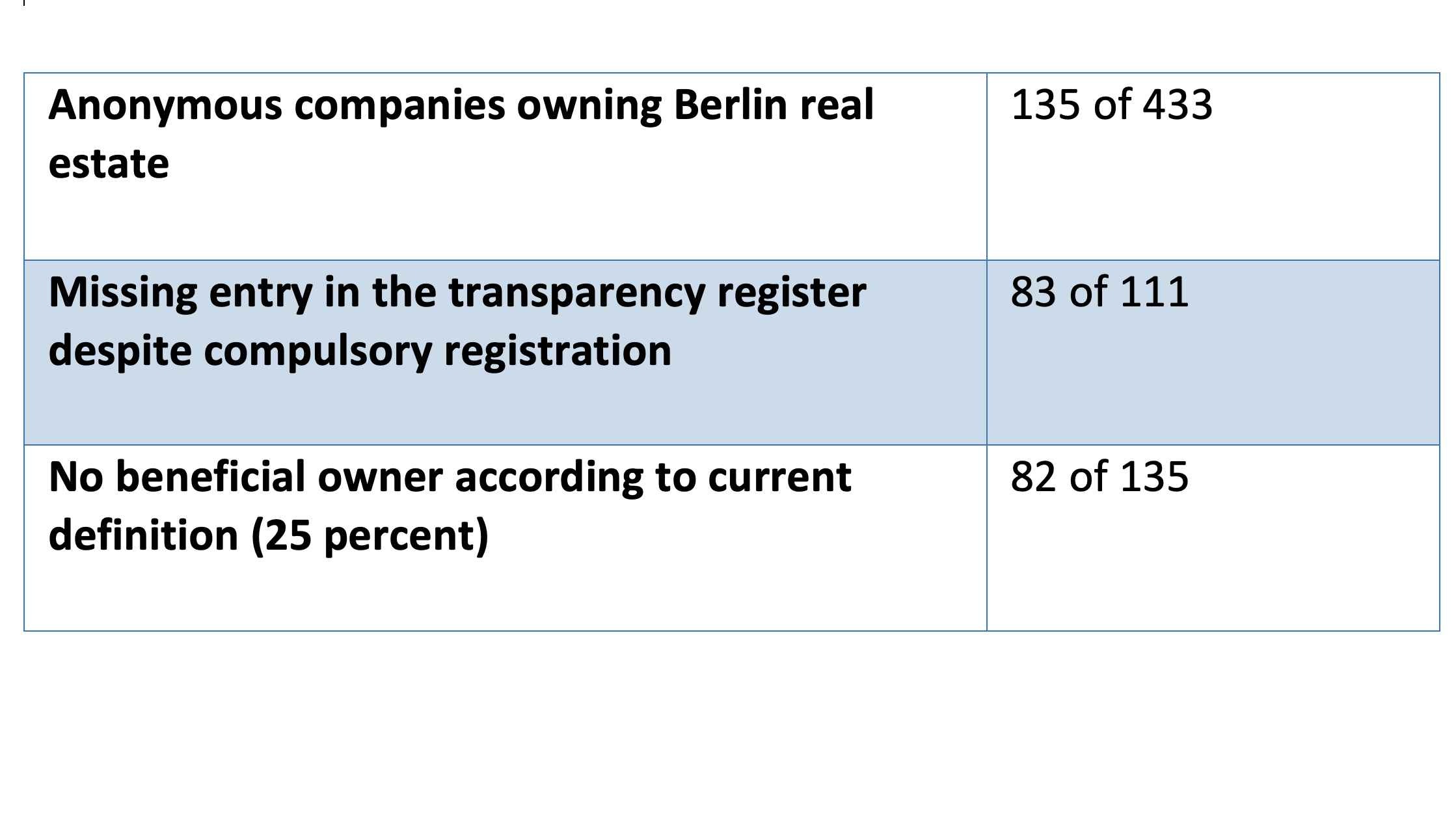

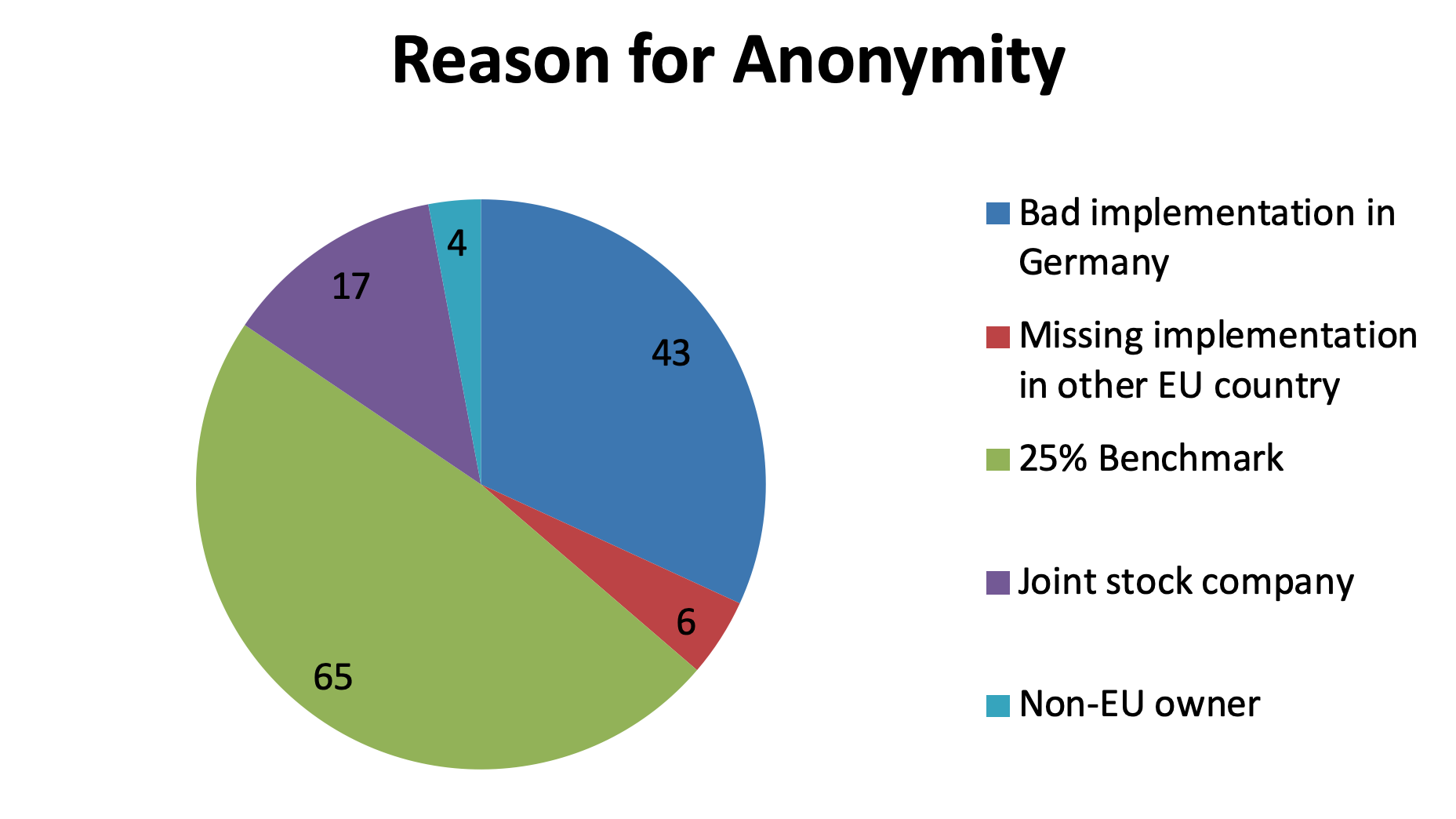

Under these circumstances, the new rule forcing foreign companies to register in the beneficial ownership register is purely symbolic and easily circumvented. Out of 433 companies owning real estate in Berlin analysed for the study, 135 remained anonymous. Out of 111 relevant cases—i.e. where this beneficial owner was not already know through the German company registers—the German beneficial ownership registry contained no entry in 83 cases and a real beneficial owner only in seven cases. In at least 82 out of the 135 cases, the real owners remained anonymous using joint stock companies and investment funds that ensure that none of them surpasses the limit of 25 percent to register as a beneficial owner.

Germany vs. the EU: The State of Play of Beneficial Ownership Registers

Although beneficial ownership registers are obligatory in the EU since 2017 and their publication was due at the beginning of 2020, only six countries (UK, Denmark, Luxembourg, Latvia, Slovenia, Bulgaria) had made their register freely accessible by then. Seventeen countries (like the Netherlands or Cyprus) do not even have a beneficial ownership register yet, or haven’t made it public (like France or Spain).[2] Germany created the register in 2017 and made it public by 2020 but there are two big issues that hamper the usefulness of the register:

First, Germany is one of only four countries (with Malta, Sweden, Norway) that don’t make the register mandatory. On top of that, instead of integrating the beneficial ownership register with the existing ones (like Denmark or the UK) Germany (like Austria or Luxembourg) opted to create a separate register that is badly integrated with the existing ones. In theory companies that already register their beneficial owners in Germany are spared of additional bureaucracy. In practice this doesn’t work. Because limited companies already have to publish all! shareholders in the company register, one typical real estate owner—Germans owning the real estate through German companies—are fully transparent. But there are also many foreign companies that hold shares of German real estate companies and whose beneficial owner consequently cannot be found in the German registers. Nearly all of these German companies failed to register in the German beneficial ownership register. Because of the bad integration of the two registers, the oversight body is unable to efficiently identify companies with foreign shareholders not registered in Germany.

Second, a significant share of Berlin real estate is owned by joint stock companies, investment funds or companies claiming to have no beneficial owner above the 25 percent benchmark of the EU definition. As a German joint stock company they have to publish anyone owning more than 3 percent of the shares and record ownership in the internal, non-public shareholder register—but they often record and know only the name of the wealth manager or the bank administering their shares rather than the beneficial owner. Many of the investment funds are structured as a combination of Cayman Island partnerships and Luxembourg SCSp—which means they do not register their investors in any of the existing registers.

Finally, cases such as Seychelles Limited or the Liechtenstein trust investing in German real estate through Luxembourg most clearly demonstrate the limits of the beneficial ownership register. While Seychelles Limited simply claims to have no beneficial owner—without any chance to verify that claim or to rule out that this is achieved through a straw person, through setting up protected cell companies or simply lying—the Luxembourg company owned by the Liechtenstein trust lists three lawyers from Liechtenstein as “fiduciary” beneficial owners, but without even naming the trust or the vehicle through which they exercise this fiduciary duty, making it impossible to investigate further or even to send a request for mutual legal assistance to Liechtenstein.

[1] In addition, German land registers are accessible only after proof of a legitimate interest. That’s why—instead of doing a full analysis or a random sample—the study was based on owners identified through a crowd-based collection of ownership data from tenants, journalists and local politicians.

[2] For a good overview see https://www.globalwitness.org/en/campaigns/corruption-and-money-laundering/anonymous-company-owners/5amld-patchy-progress/ . More detailed country profiles can be found at: https://www.pwc.nl/nl/assets/documents/the-ubo-register-update-december-2019.pdf.